- U.S. households are spending more on housing, food, gas, transportation and medical care and falling deeper into the red.

- From credit cards to car loans, the average family now owes $155,622.

Higher prices are already taking a toll.

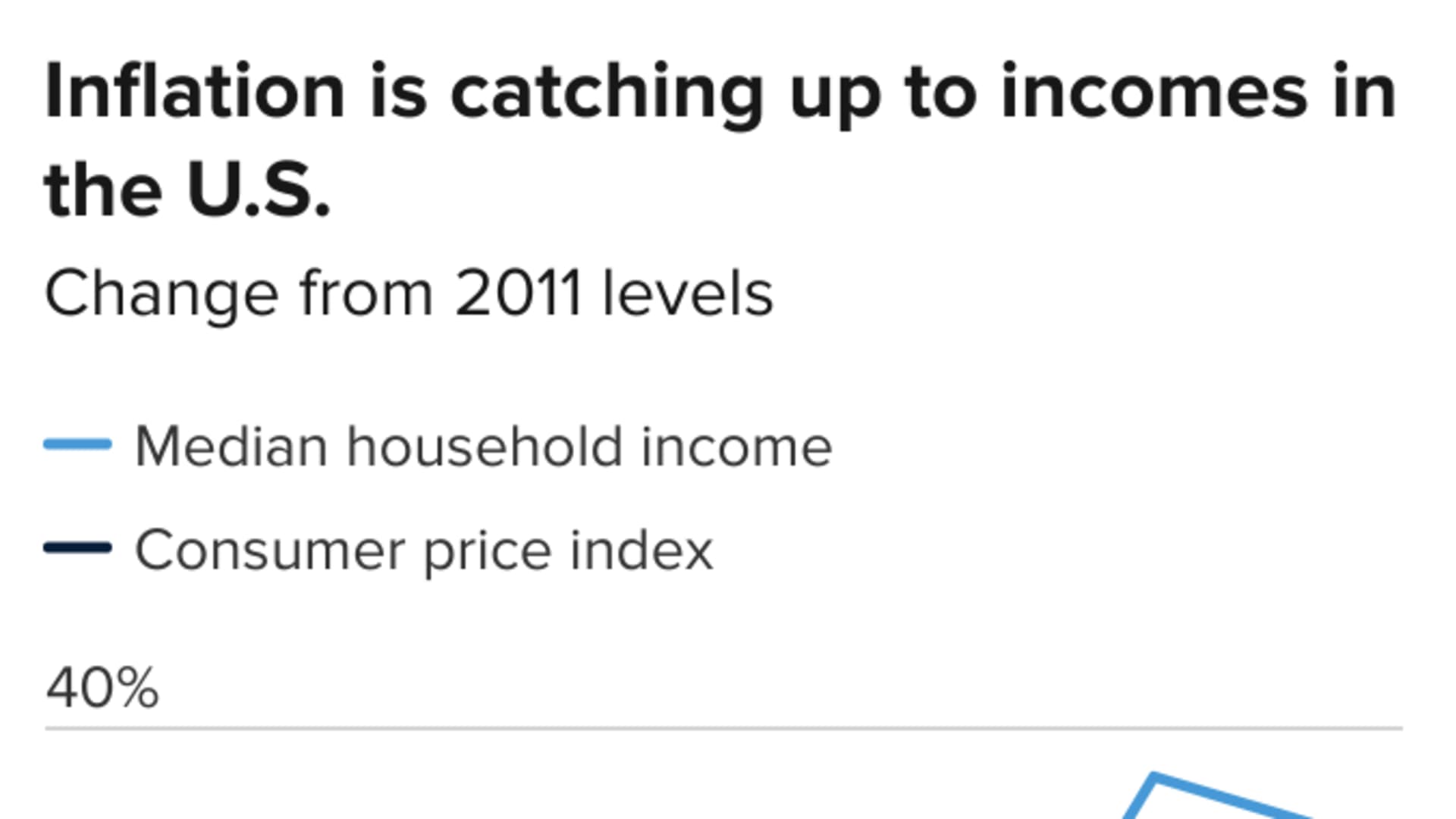

As consumers pay more for everything from groceries to gasoline, household income is failing to keep pace with a higher overall cost of living, according to recent reports.

Get San Diego local news, weather forecasts, sports and lifestyle stories to your inbox. Sign up for NBC San Diego newsletters.

Over the past two years, median income fell 3% while the cost of living rose nearly 7%, due, in part, to rising housing and medical costs.

More than three-quarters of Americans, or 78%, have received some form of pandemic relief since March 2020, which either went toward buying necessities, savings or paying down debt, according to a NerdWallet poll of more than 2,000 adults.

Money Report

And yet, more than one-third said their household financial situation has gotten worse over the past year.

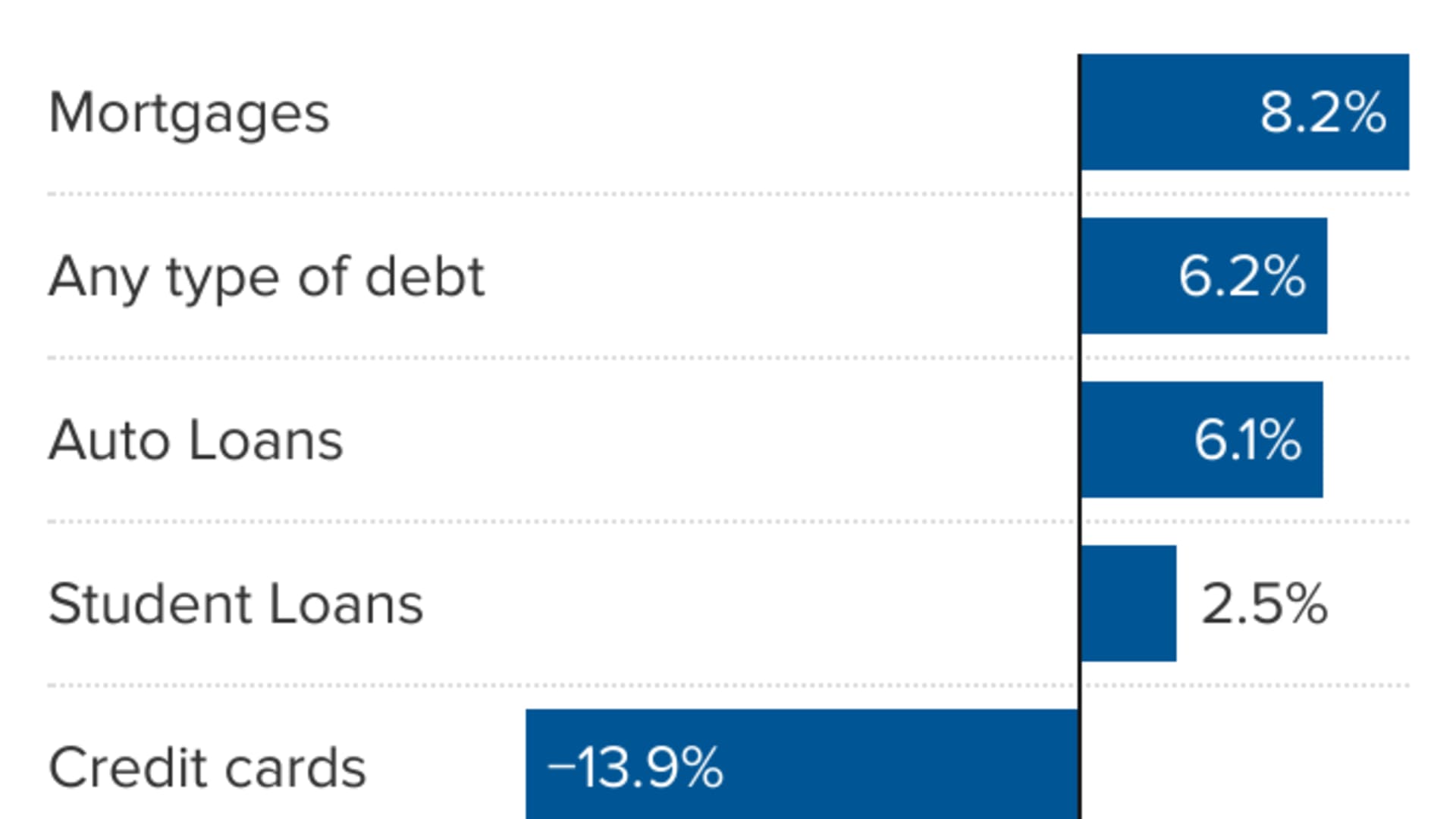

After Americans paid off a record $83 billion in credit card debt, credit card balances are on the rise again, along with mortgage, auto and student loan debt.

"The past year and a half was already tough for the millions of Americans who lost jobs," said Sara Rathner, NerdWallet's credit cards expert. "Now, we're faced with rising costs for much-needed items — food, housing, gas, transportation and medical care.

"It remains difficult for many to catch up."

The average U.S. household with debt now owes $155,622, or more than $15 trillion altogether, including debt from credit cards, mortgages, home equity lines of credit, auto loans, student loans and other household obligations — up 6.2% from a year ago.

More from Personal Finance:

10 things that will be more expensive in 2022

Your best money moves before interest rates rise

Do you think you have a spending problem?

While most federal relief measures to help individuals and families — namely expanded unemployment benefits and stimulus checks — are no longer in effect, it is expected that there will be bigger wage increases in 2022.

The Conference Board is predicting a 3.9% jump in wage costs for firms, including pay for new hires. That's the highest rate since 2008.

For those in need of more urgent assistance, Supplemental Nutrition Assistance Program benefits have been increased and there continues to be billions of dollars in federal rental assistance accessible to tenants who've fallen behind.

The Biden administration also announced last month that the payment pause for federal student loan borrowers will be extended until May.