A customer moves through the check out lane with his groceries at a Costco Wholesale store on April 3, 2024 in Colchester, Vermont.

- The Federal Reserve held rates steady at the end of its two-day meeting Wednesday, delaying the start of rate cuts and any relief from sky-high borrowing costs.

- For consumers, it generally won't get less expensive to carry credit card debt, buy a house or purchase a car.

- "Prioritizing debt repayment, especially of high-cost credit card debt, remains paramount as interest rates promise to remain high for some time," says Greg McBride, Bankrate's chief financial analyst.

The Federal Reserve announced Wednesday it will leave interest rates unchanged as inflation continues to prove stickier than expected.

However, the move also dashes hopes that the Fed will be able to start cutting rates soon and relieve consumers from sky-high borrowing costs.

Get San Diego local news, weather forecasts, sports and lifestyle stories to your inbox. Sign up for NBC San Diego newsletters.

The market is now pricing in one rate cut later in the year, according to the CME's FedWatch measure of futures market pricing. It started 2024 expecting at least six reductions, which was "completely fantasy land," said Greg McBride, chief financial analyst at Bankrate.com.

That change in rate-cut expectations leaves many households in a bind, he said. "Certainly from a budgetary standpoint, not only is inflation still high but that is on top of the cumulative increase in prices over the last three years."

"Prioritizing debt repayment, especially of high-cost credit card debt, remains paramount as interest rates promise to remain high for some time," McBride said.

Money Report

More from Personal Finance:

Cash savers still have an opportunity to beat inflation

Here's what's wrong with TikTok's viral savings challenges

The strong U.S. job market is in a 'sweet spot,' economists say

Inflation has been a persistent problem since the Covid-19 pandemic, when price increases soared to their highest levels since the early 1980s. The Fed responded with a series of interest rate hikes that took its benchmark rate to its highest level in more than 22 years.

The federal funds rate, which is set by the U.S. central bank, is the rate at which banks borrow and lend to one another overnight. Although that's not the rate consumers pay, the Fed's moves still affect the borrowing and savings rates they see every day.

The spike in interest rates caused most consumer borrowing costs to skyrocket, putting many households under pressure.

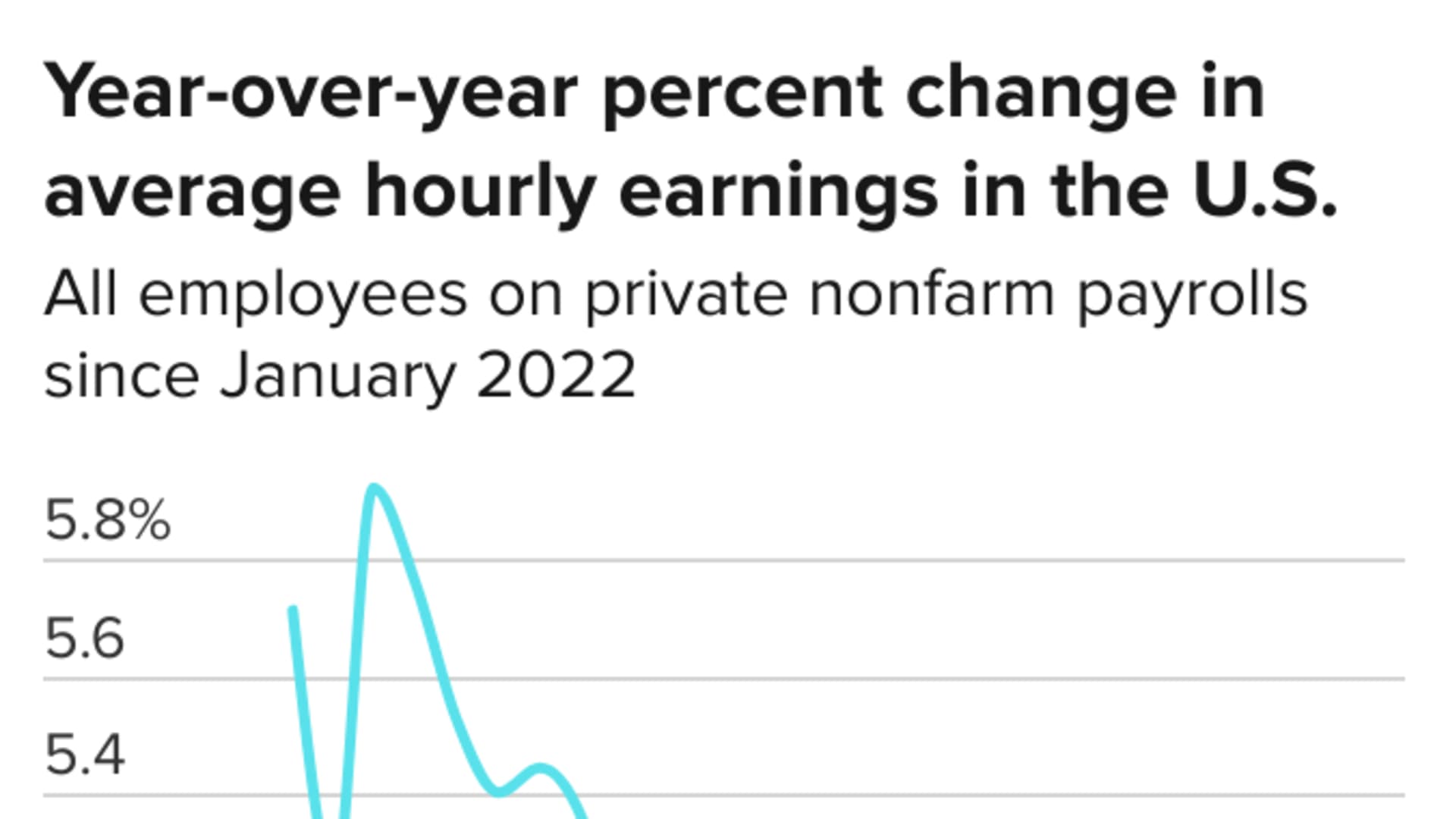

Increasing inflation has also been bad news for wage growth, as real average hourly earnings rose just 0.6% over the past year, according to the Labor Department's Bureau of Labor Statistics.

Even with possible rate cuts on the horizon, consumers won't see their borrowing costs come down significantly, according to Columbia Business School economics professor Brett House.

"Once the Fed does cut rates, that could cascade through reductions in other rates but there is nothing that necessarily guarantees that," he said.

From credit cards and mortgage rates to auto loans and savings accounts, here's a look at where those rates could go in the second half of 2024.

Credit cards

Since most credit cards have a variable rate, there's a direct connection to the Fed's benchmark. In the wake of the rate hike cycle, the average credit card rate rose from 16.34% in March 2022 to nearly 21% today — an all-time high.

Annual percentage rates will start to come down when the central bank reduces rates, but even then they will only ease off extremely high levels. With only a few potential quarter-point cuts on deck, APRs aren't likely to fall much, according to Matt Schulz, chief credit analyst at LendingTree.

"If Americans want lower interest rates, they're going to have to do it themselves," he said. Try calling your card issuer to ask for a lower rate, consolidating and paying off high-interest credit cards with a lower-interest personal loan or switching to an interest-free balance transfer credit card, Schulz advised.

Mortgage rates

Although 15- and 30-year mortgage rates are fixed, and tied to Treasury yields and the economy, anyone shopping for a new home has lost considerable purchasing power, partly because of inflation and the Fed's policy moves.

The average rate for a 30-year, fixed-rate mortgage is just above 7.3%, up from 4.4% when the Fed started raising rates in March 2022 and 3.27% at the end of 2021, according to Bankrate.

"Going forward, mortgage rates will likely continue to fluctuate and it's impossible to say for certain where they'll end up," noted Jacob Channel, senior economist at LendingTree. "That said, there's a good chance that we're going to need to get used to rates above 7% again, at least until we start getting better economic news."

Auto loans

Even though auto loans are fixed, payments are getting bigger because car prices have been rising along with the interest rates on new loans, resulting in less affordable monthly payments.

The average rate on a five-year new car loan is now more than 7%, up from 4% in March 2022, according to Edmunds. However, competition between lenders and more incentives in the market lately have started to take some of the edge off the cost of buying a car, said Ivan Drury, Edmunds' director of insights.

"Any reduction in rates will be especially welcome as there is an increasingly higher share of consumers with older trade-ins that have sat out the market madness waiting for an automotive landscape that looks more like the last time they bought a vehicle six or seven years ago," Drury said.

Student loans

Federal student loan rates are also fixed, so most borrowers aren't immediately affected. But undergraduate students who took out direct federal student loans for the 2023-24 academic year are now paying 5.50%, up from 4.99% in 2022-23 — and any loans disbursed after July 1 will likely be even higher. Interest rates for the upcoming school year will be based on an auction of 10-Year Treasury notes later this month.

Private student loans tend to have a variable rate tied to the prime, Treasury bill or another rate index, which means those borrowers are already paying more in interest. How much more, however, varies with the benchmark.

For those struggling with existing debt, there are ways federal borrowers can reduce their burden, including income-based plans with $0 monthly payments and economic hardship and unemployment deferments.

Private loan borrowers have fewer options for relief — although some could consider refinancing once rates start to come down, and those with better credit may already qualify for a lower rate.

Savings rates

While the central bank has no direct influence on deposit rates, the yields tend to be correlated to changes in the target federal funds rate.

As a result, top-yielding online savings account rates have made significant moves and are now paying more than 5.5% — above the rate of inflation, which is a rare win for anyone building up a cash cushion, McBride said.

"The mantra of higher-for-longer interest rates is music to the ears of savers who will continue to enjoy inflation-beating returns on safe-haven savings accounts, money markets and CDs for the foreseeable future," he said.

Currently, top-yielding certificates of deposit pay over 5.5%, as good as or better than a high-yield savings account.