- If you take no action, you'll automatically remain enrolled in your current plan.

- The specifics of both Advantage Plans and Part D prescription drug options vary from year to year and plan to plan.

- Those changes can affect things like your premiums, copays and out-of-pocket maximums, as well as covered services and participating providers.

You don't have much time left to give your Medicare coverage a yearly checkup and make changes for 2021.

The program's annual enrollment period ends Dec. 7. If you take no action, you'll automatically remain enrolled in your current plan. However, if you pass on the opportunity to see whether a better option exists, it could cost you.

"We're finding many circumstances where changing plans does benefit our policyholders," said Danielle Roberts, co-founder of insurance firm Boomer Benefits. "But sometimes we find that someone is already in the best plan for them next year … and they can let their current plan auto-renew."

More from Personal Finance:

Some easy ways for retirees to reduce their tax hit

Medicare Part B premiums will rise by 2.7% in 2021

What to watch for if Medigap is part of your coverage

In simple terms, this annual fall open enrollment period is for adding or changing coverage related to an Advantage Plan (Medicare Part C) and prescription drugs (Part D). You can switch, add or drop those parts of your coverage.

Of the nearly 63 million people enrolled in Medicare — the majority of whom are age 65 or older — about a third choose to get their benefits through Advantage Plans, which are offered by private insurers.

Money Report

The remainder stick with original Medicare: Part A (in-patient coverage) and Part B (outpatient care). Those beneficiaries often pair that with a standalone Part D plan and/or a Medicare supplemental plan (aka Medigap), both of which also are offered by private insurance companies.

For 2021, the average beneficiary has access to 33 Advantage Plans, research from the Kaiser Family Foundation shows. Altogether, 3,550 such plans will be available, up 13% from this year. This means that even if you haven't wanted a different option in the past, the situation could be different for 2021.

While the insurers are regulated, the specifics can vary greatly from plan to plan, county to county and year to year. Changes can affect coverage aspects such as premiums, deductibles, co-pays, covered services, and participating doctors and other providers.

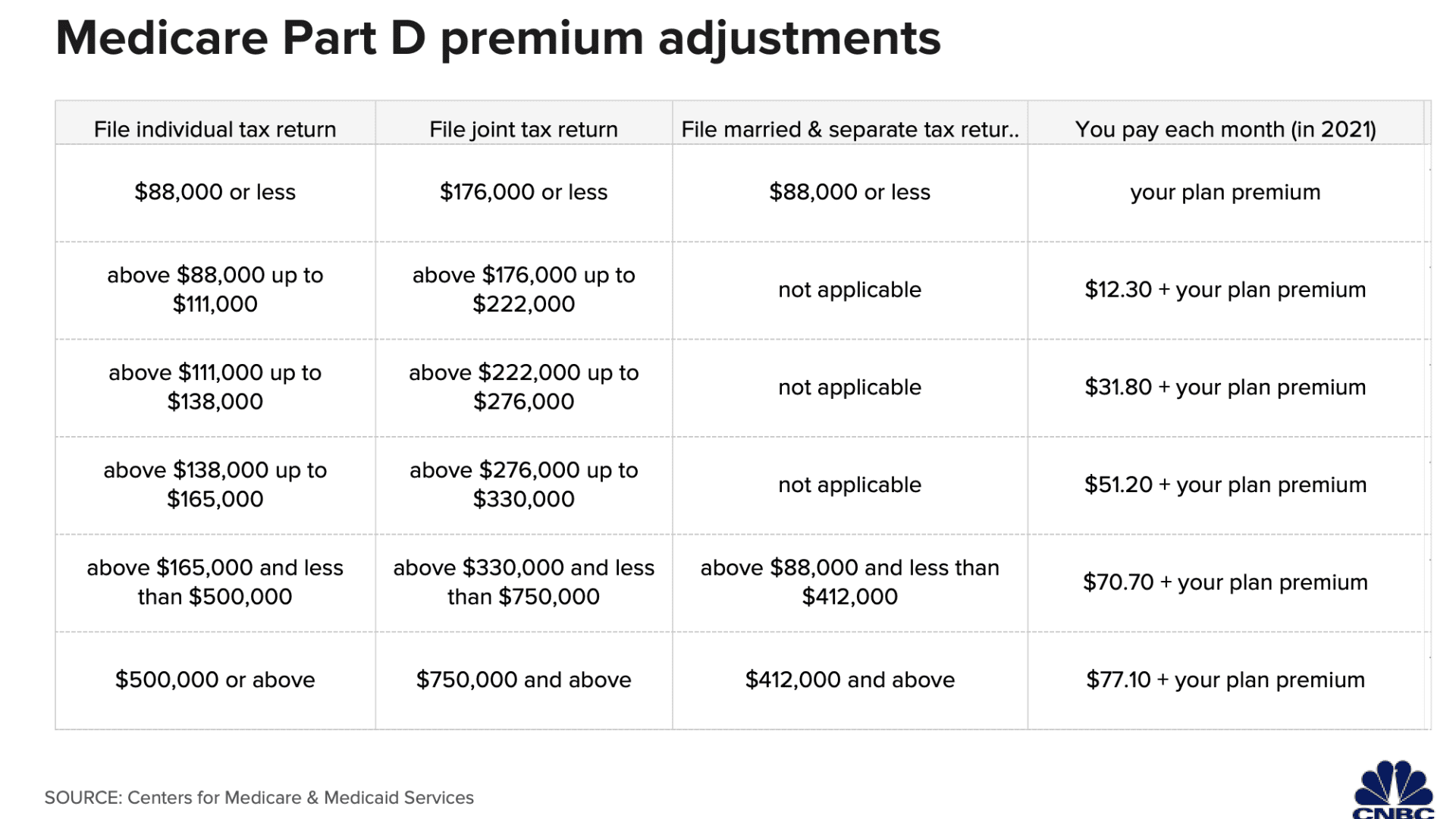

Be aware, as well, that the standard Part B monthly premium is higher next year ($148.50 vs. $144.60 in 2020), as are the extra amounts paid by higher-income beneficiaries for Parts B and D premiums (see charts).

Also, whether via an Advantage Plan or standalone Part D plan, Roberts said, it's important to make sure the plan covers your prescriptions. Sometimes your existing coverage will remain the best option, but other times there's another plan that would be less costly.

"You don't want to go to the pharmacy in January and discover a drug you've been paying $40 for is now $400," Roberts said.

With Advantage Plans, other terms of your coverage may change, as well. For instance, the out-of-pocket limit in 2021 will be $7,550, up from $6,700 this year, Roberts said.

If you pick an Advantage Plan during fall enrollment and realize afterward that it's not a good fit, you can switch to another one or back to original Medicare (and pick up a stand-alone Part D plan) between Jan. 1 and March 31.

You can check medication prices through the government's Medicare plan finder.

To make sure your doctor, pharmacy or preferred hospital is in-network, check with the insurance company offering the plan and confirm it with the provider.