- The pandemic sparked a wave of older workers retiring in 2020, according to Pew Research.

- However, many early retirees don’t have the resources for making the jump.

- Those weighing early retirement need to review their income, savings and health care coverage, financial experts say.

After a year of grappling with the pandemic, many baby boomers have made changes to their retirement plans.

Mary Ann Sergeant, 65, spent more than 15 years working as a pharmacy technician at Anna Jaques Hospital in Newburyport, Massachusetts.

She wasn't planning to retire from the community hospital for another year or two. But the strains as a frontline health worker became too much, and she retired early in December.

Get San Diego local news, weather forecasts, sports and lifestyle stories to your inbox. Sign up for NBC San Diego newsletters.

"I felt like there was no other decision that I could have made at that time," she said. "I really didn't want to leave."

More from Personal Finance:

How Biden's capital gains proposal may hit middle-class home seller

Biden's inherited real estate tax may impact more people than just the wealthy

How Biden's real estate tax plan may hit smaller property investors

Sergeant isn't alone in her jump to early retirement.

Money Report

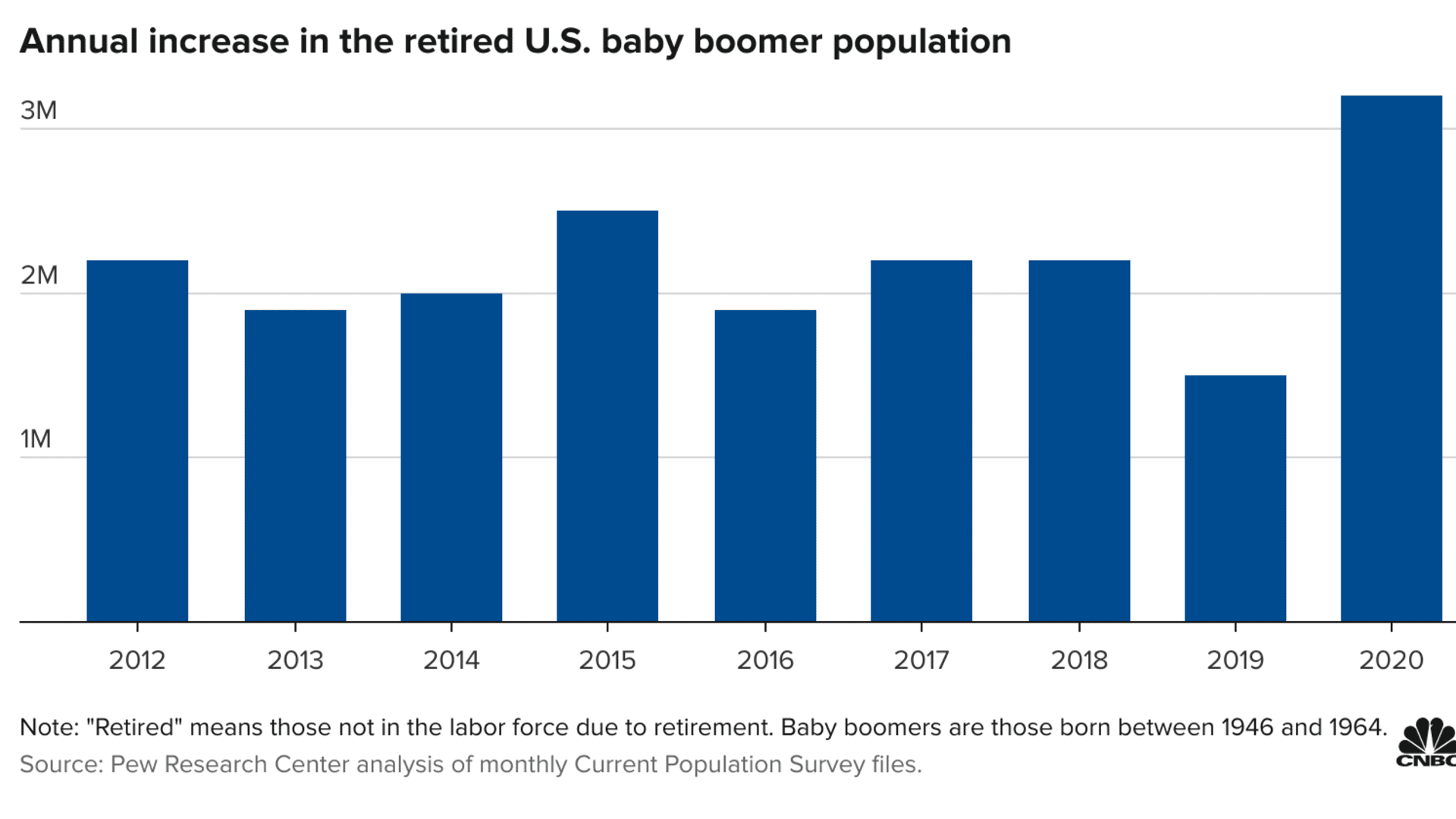

Some 28.6 million boomers said they were now out of the workforce due to retirement as of the third quarter of 2020, out of total national cohort of about 71.6 million. That is 3.2 million more than those who said they were retired during the same period in 2019, according to a Pew Research report.

"Maybe for some, they faced their mortality and figured 'why am I going to work if my life expectancy could be curtailed by this pandemic?' I'm sure that hit a lot of people," said Paul Gaudio, certified financial planner and wealth planning strategist at Bryn Mawr Trust in Princeton, New Jersey.

While Sergeant's leap was due to the rigorous demands of healthcare, boomers nationwide share the sentiment of wanting to retire early, particularly women.

Americans expecting to work past age 67 dipped to a low of 32.9% in March, a New York Federal Reserve survey uncovered.

"The biggest risk of retiring early is that you have to make your savings last longer," said Jude Boudreaux, CFP and partner at The Planning Center in New Orleans.

He said leaving the workforce too soon may put extra pressure on an investment portfolio, depending on how much someone has saved.

"You're solely dependent on your financial assets, and hopefully, that base is sufficient to accommodate the standard of living for a normal life expectancy," said Gaudio.

After crunching the numbers, Sergeant knew early retirement was within reach.

She paid off her home in Merrimac, Massachusetts, and made her last car payment three years ago.

She also has retirement savings in her 401(k) and 403(b) plans from jobs throughout her career, along with a "very small pension" from the hospital.

"I knew financially I could mostly do it, and that was a big part," she said.

Many older workers aren't as fortunate, however.

Just over half of households with workers aged 55 to 64 have retirement accounts, and their median value is $134,000, a report from the Center on Budget and Policy Priorities showed.

These balances may translate to $7,500 per year for men and 7% less for women, who typically live longer, assuming they start withdrawals at 65.

Applying for Social Security

"I think the most difficult question is when to take Social Security," said Boudreaux.

While retirees may receive checks as early as 62, there's an incentive to delay payments.

Those who don't tap Social Security until full retirement age may receive higher monthly checks for life, depending on their birth year. A retiree may lock in a bigger payment through age 70.

For example, those born in 1957 have a full retirement age of 66 and six months.

If they qualify for $1,000 in benefits and start collecting at 62, they would only receive $725 per month — a 27.5% reduction for life, according to the Social Security Administration.

There's roughly an 8% reduction per year or two-thirds percent per month, Boudreaux said.

Retirees lose $3.4 trillion in Social Security income, an average of $111,000, by claiming benefits too early, according to a report from investment firm United Capital.

Delaying until full retirement age offers the highest payout, but that isn't an option for all retirees.

Sergeant, for example, started receiving Social Security checks in January, six months before her full retirement age.

Luckily, her retirement savings and small pension may pad her reduced payments. She also works part-time at the hospital at least once every month.

Bridging the gap to Medicare

Another significant retirement expense is the cost of health care.

The average 65-year-old couple may spend a whopping $295,000 in retirement, not including long-term care, Fidelity estimated in 2020.

For some workers, retiring early means parting with their workplace health insurance.

After years of coverage through her employer, Sergeant had to apply for Medicare and a supplemental plan. With offices closed because of the pandemic, she described it as the biggest challenge of retiring.

But retirees under age 65 won't qualify for Medicare and may have costly options to navigate.

"Make sure you're clear about what the costs and realities are of purchasing your own policy through an exchange or broker," said Boudreaux.

Some retirees bridge the gap through a spouse's workplace insurance, COBRA or even their company's health benefits for retirees. But company retiree plans are less likely to be an option, according to a survey from Kaiser Family Foundation.

"Anybody that takes the proverbial leap before that needs to account for the medical costs, whether it's for him or herself, and potentially a spouse," Gaudio said. "Those numbers can be staggering."

Consider a 'test retirement'

Boudreaux said there's also a risk of dashing to retire, only to feel bored later.

Some retirees may decide to "unretire," making the shift back to the workforce.

Thirty-nine percent of workers age 65 and older have already retired once, a report from nonprofit research firm RAND Corporation found.

"If this is stress- and burnout-related, I'd really encourage them to take a step back before taking a step away," he said.

He suggests trying a leave of absence and scheduling three or four weeks off for a "test retirement." If they feel refreshed after that, it may be possible to continue working a little longer.

Fortunately, Sergeant has plenty of ways to stay busy in retirement.

After an unrelenting year, she's relieved to spent time winding down at home, where she enjoys reading. While many businesses haven't reopened, she's eager to start practicing yoga or take some classes.

She also enjoys working part-time at the hospital once every month.

"That's one good thing about our jobs. We can do that and ease our way out," she said.