It's easy to get twisted up around money. In fact, most Americans are.

The pandemic has been stressful, with concerns about health, work, and finances. But even before the pandemic, the average American was financially stressed. In good times and bad, Americans are stressed about money. In pre-pandemic 2019, six out of 10 Americans identified money as a significant source of stress in their lives.

We live in one of the richest countries in the world and in the most prosperous times in human history. Our standard of living is higher than ever before. So why are we so stressed about money?

The basics of personal finance are simple: save and invest for the future and don't spend more than you make. However, this is where we struggle most. The average credit card debt in 2019 was $6,200 with a savings rate of 7.6% in 2019. Our financial stress is not entirely dependent on our financial circumstances. For example, despite our stress during the pandemic, credit card debt went down to an average of $5,315 in 2020 and savings rates when up to 13.7%.

Get San Diego local news, weather forecasts, sports and lifestyle stories to your inbox. Sign up for NBC San Diego newsletters.

Financial literacy is important. However, financial health is more than just knowing what we should do. For example, everyone knows they shouldn't rack up a bunch of revolving credit card debt and they should be saving more for the future. For the most part, we already know what we should be doing. So why can't we change our behaviors?

To straighten out our twisted financial lives we need to first understand our relationship with money. This is where your financial psychology comes in.

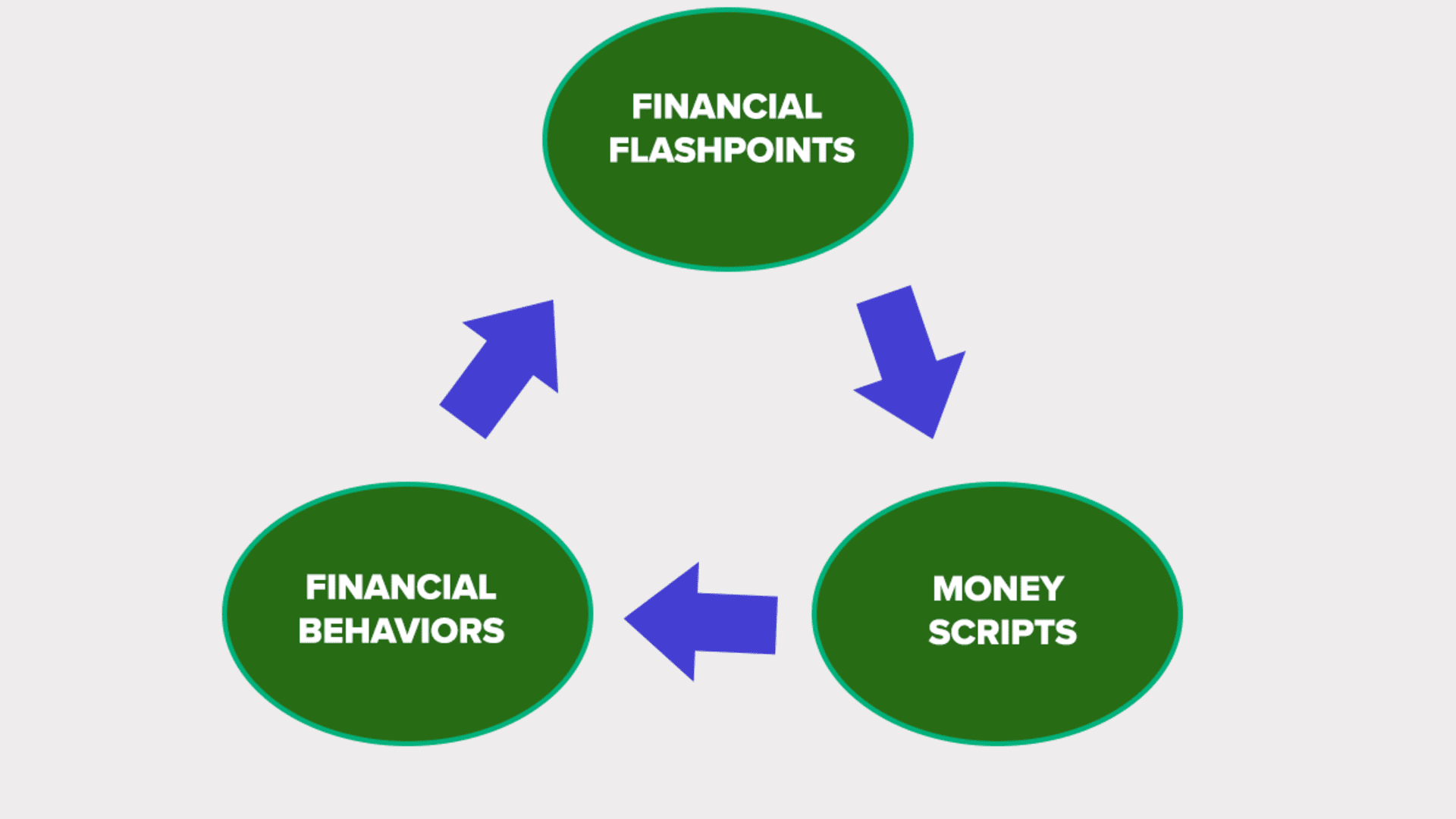

Your financial psychology consists of three components: your financial flashpoints, your money scripts, and your financial behaviors and outcomes. Understanding the intersection of these three components of your financial psychology can help you transform your relationship with money.

Money Report

1. Your financial flashpoints

Financial flashpoints are experiences around money that leave a lasting imprint on your financial life. They can include things as dramatic as living through the Great Depression, to growing up poor, to watching your parents fight about money. Sometimes we experienced financial flashpoints directly, and sometimes their impact is felt for generations. Our financial flashpoints lead to our money scripts, which are our attempts to make sense of how money works in our lives and in the world. To help you identify your financial flashpoints, reflect on the following questions:

- What was it like for you growing up around money?

- What was your socioeconomic class? How did you feel about it?

- What is your earliest memory around money?

- What is your most joyful money memory?

- What is your most painful money memory?

2. Your money scripts

We develop money scripts – our beliefs about money – in our attempts to make sense of our financial flashpoints. Many of our scripts around money lie outside of our conscious awareness. They are passed down to us by our parents, our grandparents, and our culture. They are like scripts in a play, often written for us by someone else. Some of these scripts serve us well while others set us up for chronic financial failure. Many studies have linked our money scripts to our financial behaviors and outcomes. To identify your beliefs about money you can take the Klontz Money Script Inventory assessment, or reflect on the following questions:

- What 3 things did your mother teach you about money?

- What 3 things did your father teach you about money?

- What did you learn about money from your culture?

- What beliefs about money did you learn from your socioeconomic group?

- How have these beliefs helped you? How have they hurt you?

- What is a more helpful way to think about money?

3. Your financial behaviors and outcomes

Your financial flashpoints lead to the formation of your money scripts. Your beliefs about money, in turn, predict your financial behaviors. Studies have found that money scripts are associated with financial behaviors and outcomes, including credit card debt, income, socioeconomic status in childhood, net worth, overspending, financially enabling others, and many other financial behaviors. The craziest and most self-destructive financial behaviors make perfect sense when you understand the financial flashpoints and money scripts that drive them.

Your financial problems are not the result of you being crazy, lazy, or stupid. Understanding your financial psychology will help you make sense of your relationship with money. When you identify your financial flashpoints and your resulting beliefs about money, your financial outcomes will make perfect sense. When you take the time to understand your financial psychology and challenge and change the money scripts that are holding you back, you can transform your financial life.

—By Bradley T. Klontz, Psy.D., CFP, expert in financial psychology, behavioral finance, and financial planning. Klontz is managing principal of Your Mental Wealth Advisors and a founder of the Financial Psychology Institute. Klontz is a member of the CNBC Financial Wellness Council.

SIGN UP: Money 101 is an 8-week learning course to financial freedom, delivered weekly to your inbox.

CHECK OUT: Nearly half of Americans selling their homes don't plan to buy another: Here's what they're doing instead via Grow with Acorns+CNBC

On September 9, CNBC + Acorns Invest in You: Ready. Set. Grow. will remove the stigma of discussing financial anxiety and provide Americans direct access to financial and psychology experts who will answer their most pressing questions about handling their money stress and achieving financial well-being.

Invest in You: Mind Over Money will stream on CNBC's Facebook page on Thursday, September 9 from 1-2p ET.

To register for this free, virtual event, go to cnbc.com/mindovermoneyevent.

Disclosure: NBCUniversal and Comcast Ventures are investors in Acorns.