- Half of parents with a child over 18 provide them with at least some financial support, according to a report.

- For parents, however, supporting grown children can be a substantial drain at a time when their own financial security is at risk.

Throughout the pandemic, many adults turned to a likely safety net: their parents.

From buying food to paying for their cell phone plan or covering health and auto insurance, half of parents with a child over 18 provide them with at least some financial support, according to a report by Savings.com.

These parents are shelling out roughly $1,000 a month, on average, on such expenses, the report found.

Get San Diego local news, weather forecasts, sports and lifestyle stories to your inbox. Sign up for NBC San Diego newsletters.

More from Personal Finance:

Many workers are unhappy with their pay

More Americans feel cash-strapped as inflation spikes

Sacrifices young adults have made to pay their student loans

Young adults just starting out have faced significant financial hurdles over the last few years, including an uneven job market, hefty student loan bills from school and soaring housing costs.

In 2020, the share of those living with their parents (often referred to as "boomerang kids") temporarily spiked to a historic high.

Money Report

And yet, 62% of adult children living at home don't contribute to household expenses at all, Savings.com found.

Now, inflation poses new challenges for achieving financial independence.

For parents, however, supporting grown children can be a substantial drain at a time when their own financial security is at risk.

"Even with the additional responsibility of taking care of adult children, parents must also take care of themselves," said Shelly-Ann Eweka, senior director of financial planning strategy at TIAA.

"It's like when you're on an airplane, and the flight crews say if you need to wear masks because of an emergency, you need to put yours on first before helping others."

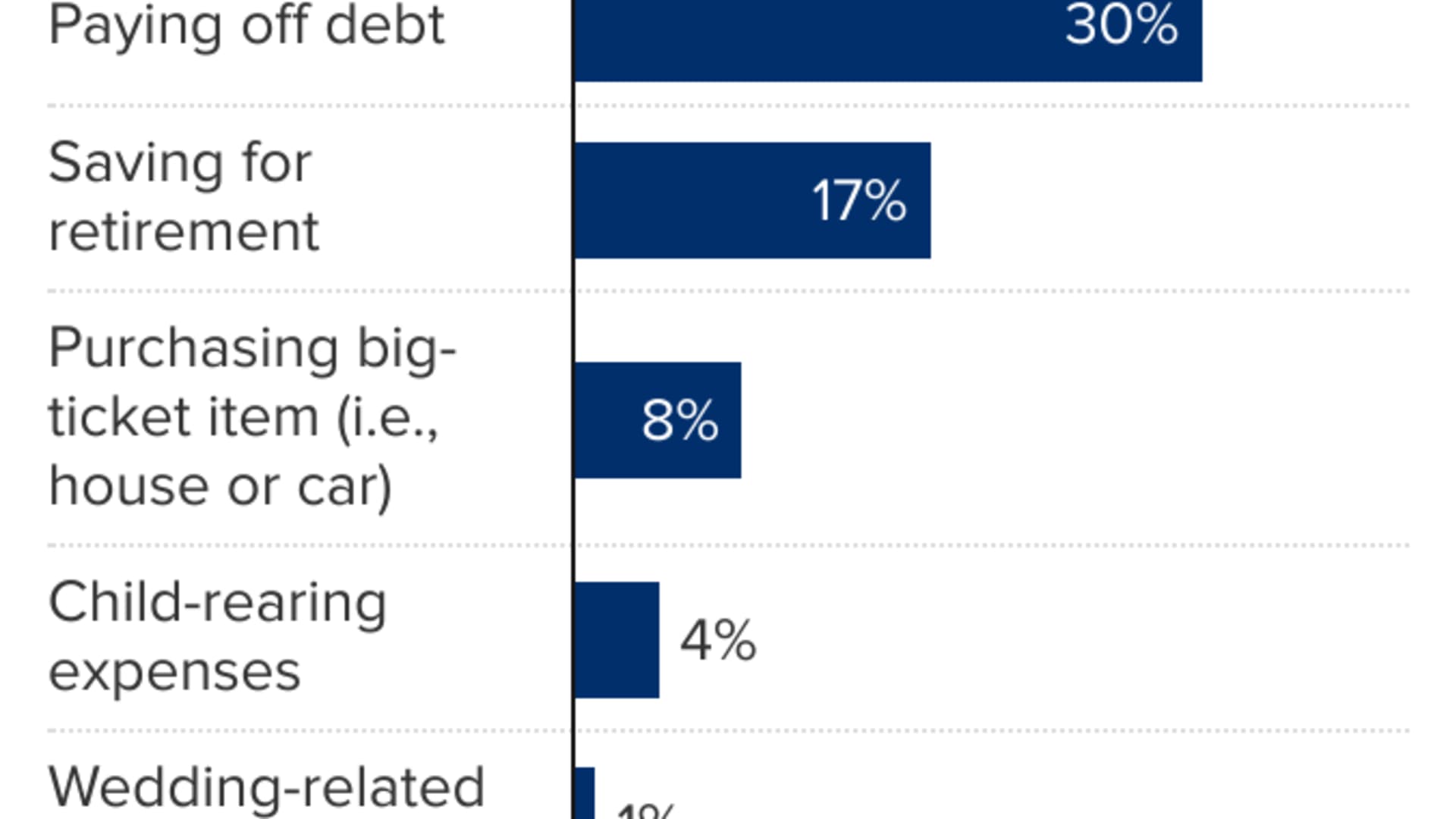

When you spend money supporting your adult children, that drains the funds you could have put toward other financial goals, such as paying off debt, saving for long-term health-care costs and retirement planning, Eweka said.

As a general rule, you should set aside money for your retirement and emergency fund first, she added.

"It's important to prioritize where your money should go."

Subscribe to CNBC on YouTube.